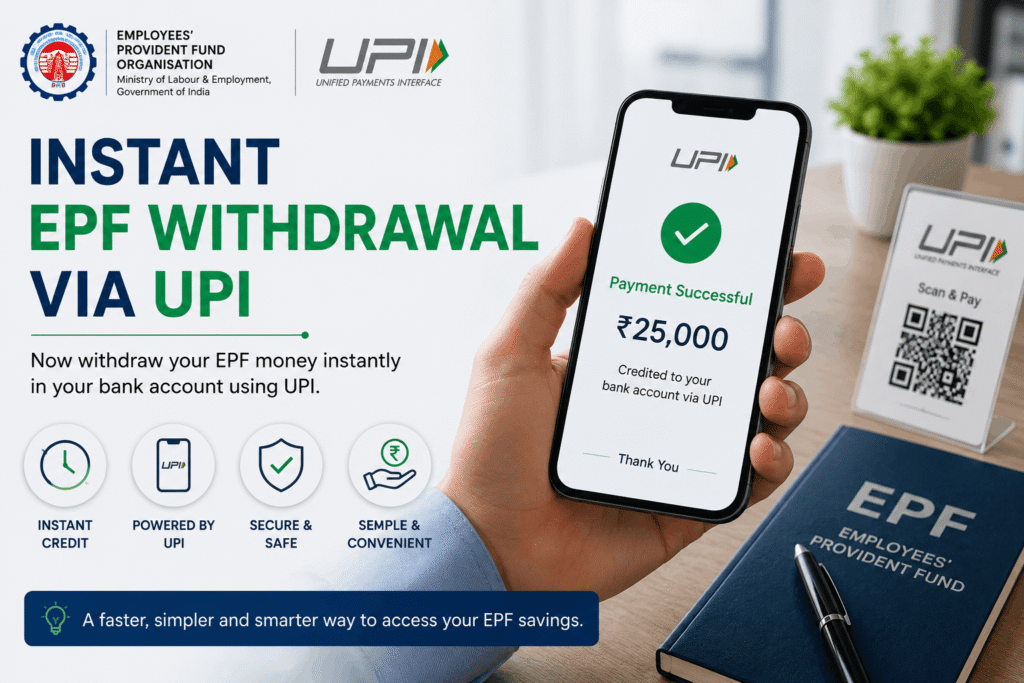

The lines separating traditional retirement savings from digital retail banking are officially blurring. The Ministry of Labour has confirmed that the testing phase for instant EPF withdrawal via UPI is complete.

Under the upcoming EPFO 3.0 framework, members will soon be able to bypass days of processing time and transfer eligible provident fund balances directly into their bank accounts via the UPI gateway.

While this brings unprecedented liquidity to employees, it introduces new structural responsibilities for business owners and strategic considerations for individual taxpayers. As a professional advisory firm, we look at this update not just as a technology upgrade, but as a fundamental shift in payroll health and personal wealth preservation.

The Mechanism: How Instant EPF Withdrawal via UPI Works

Historically, accessing your Employees’ Provident Fund (EPF) was defined by “friction by design”—an intentional hurdle to prevent people from draining their retirement nest eggs.

The new framework eliminates this friction. The operational workflow is designed to be as simple as a standard digital payment:

- Balance Check: Subscribers log in to view their clear, pre-approved “eligible withdrawal balance.”

- Authentication: Instead of relying on manual employer approvals or multi-day bank clearing batches, the subscriber enters their UPI ID.

- Instant Credit: The transaction is authenticated via a secure UPI PIN and Aadhaar-based OTP, routing the funds immediately into the individual’s seeded bank account.

To support this infrastructure, the government is also raising the electronic auto-settlement limit from ₹1 Lakh to ₹5 Lakh and introducing localized, 24/7 WhatsApp support to iron out registration glitches.

[CTA Placement 1 – Contextual] Is your company’s payroll infrastructure ready for the data stringency of EPFO 3.0? A single mismatched character in employee records can stall compliance. [Schedule a Corporate Payroll Health Check with Our Experts Today].

The Structural Guardrails: The 75/25 Balance Rule

To ensure that instant liquidity does not compromise India’s long-term social security net, the government has built strict financial guardrails into the system.

The most vital change is the 75/25 balance retention policy. Under these rules, while eligible emergency withdrawals can happen instantly via UPI, a mandatory 25% of the total balance will remain frozen to ensure the core compounding engine of the retirement fund stays alive.

A Practical Example of the New Rules

Let’s look at how this plays out in real life for an individual or an employer managing workforce inquiries:

- The Scenario: Rohan, a senior manager, faces a sudden medical emergency requiring ₹4,00,000.

- Under the Old System: Rohan would file an emergency claim under the auto-settlement route. He would wait between 3 to 7 business days, tracking the portal anxiously while hoping his bank account details matched his Universal Account Number (UAN) perfectly.

- Under the New UPI System: Because the auto-settlement limit has been increased to ₹5 Lakh, Rohan can request the ₹4,00,000 withdrawal instantly. Assuming this amount sits within his 75% eligible balance limit, he enters his UPI PIN, and the money hits his hospital-linked account in less than 60 seconds.

The Compliance & Financial Perspective: What You Need to Know

From a financial advisory perspective, this new ease of access requires careful, disciplined management.

1. For Individuals: The Compounding vs. Liquidity Trap

The EPF remains one of the most secure, high-yield debt instruments available in India, consistently offering an attractive interest rate around 8.25%.

While having instant EPF withdrawal via UPI is an incredible safety net for true crises, treating your EPF like a regular savings account destroys the power of long-term compounding. Withdrawing funds prematurely for non-emergency lifestyle expenses means missing out on tax-free, guaranteed growth that is difficult to replicate in alternative low-risk markets.

Learn more about balancing debt portfolios in our comprehensive guide on [New Income Tax Act 2025: Why Businesses Should Pay Attention Now].

2. For Business Owners: The KYC and Zero-Tolerance Data Challenge

Because this system runs on instantaneous, API-driven networks like the NPCI grid, there is zero room for manual errors. If your employees have unmatched data between their Aadhaar, PAN, Bank IFSC codes, and their EPFO portal, the UPI transaction will fail instantly. This shifts the operational burden back onto your HR and finance teams, who will have to resolve legacy data discrepancies.

Furthermore, the upcoming rollout targets beneficiaries under the Pradhan Mantri Viksit Bharat Rozgar Yojana (PMVBRY), meaning businesses must ensure flawless compliance with Direct Benefit Transfer (DBT) activations and UIDAI Face Authentication standards.

How We Can Help

Navigating structural updates in corporate compliance and personal wealth requires an authoritative, proactive approach. Our firm acts as your strategic partner to ensure these transitions are seamless.

- For Corporate Clients & Employers: We provide end-to-end payroll compliance audits, seamless UAN data remediation, and alignment with the strict requirements of EPFO 3.0 to mitigate employee friction.

- For Individual Professionals & Business Owners: We structure your comprehensive tax-saving roadmaps, helping you evaluate when to tap into liquid assets versus preserving high-yield, compounding instruments like the EPF.

Don’t let compliance errors disrupt your team’s peace of mind or invite regulatory audits. Contact our corporate advisory desk to seamlessly align your systems with the newest EPFO mandates. [Connect with a Advisory Partner]

Frequently Asked Questions (FAQs)

Q: Can I withdraw my entire EPF balance instantly through UPI? A: No. To safeguard your retirement security, the proposed framework allows you to withdraw up to 75% of your eligible balance instantly, while the remaining 25% remains frozen under existing long-term retirement guidelines.

Q: What is the new auto-settlement limit for EPF withdrawals? A: The government has increased the auto-settlement limit from ₹1 Lakh to ₹5 Lakh. This covers the vast majority of standard claims for medical emergencies, education, housing, and marriages without requiring manual human verification.

Q: Will my employer need to approve my UPI EPF withdrawal? A: Under the new system, self-certification backed by UPI PIN authentication and Aadhaar-linked OTPs minimizes the need for real-time employer attestation for eligible, automated claims. However, your master KYC data must be pre-approved and perfectly updated by your employer beforehand.

Q: Are there any tax implications for withdrawing EPF early via UPI? A: The method of withdrawal (UPI vs. traditional bank transfer) does not change tax laws. EPF withdrawals are generally tax-free if you have completed 5 continuous years of service. If you withdraw before 5 years, it may attract TDS or become taxable under specific conditions. It is highly recommended to consult a CA before making early withdrawals.

The Final Takeaway

The integration of UPI into the EPFO ecosystem is a landmark achievement for Indian public infrastructure. It grants citizens unprecedented control over their financial assets when they need it most. However, with absolute convenience comes the absolute need for financial discipline and flawless administrative compliance.

Whether you are looking to optimize your company’s payroll architecture or build a resilient personal tax strategy, our experienced team of professionals is here to guide you. [Book a Strategic Consultation Today].