From April 2026, finance teams across India may need to revisit how their payroll systems, vendor masters, and TDS workflows are configured.

The proposed restructuring of TDS and TCS provisions under the new Income Tax framework is expected to affect not only compliance reporting, but also day-to-day accounting operations. For many businesses, the challenge may not be understanding the law — it will be ensuring that accounting systems, payroll utilities, and reporting processes are updated before the first compliance cycle of FY 2026–27 begins.

While the core tax structure remains broadly unchanged, the compliance architecture surrounding withholding tax is undergoing a significant transition.

What Happens to Existing TDS & TCS Section Codes?

One of the key changes under the revised framework is the restructuring and renumbering of withholding tax provisions.

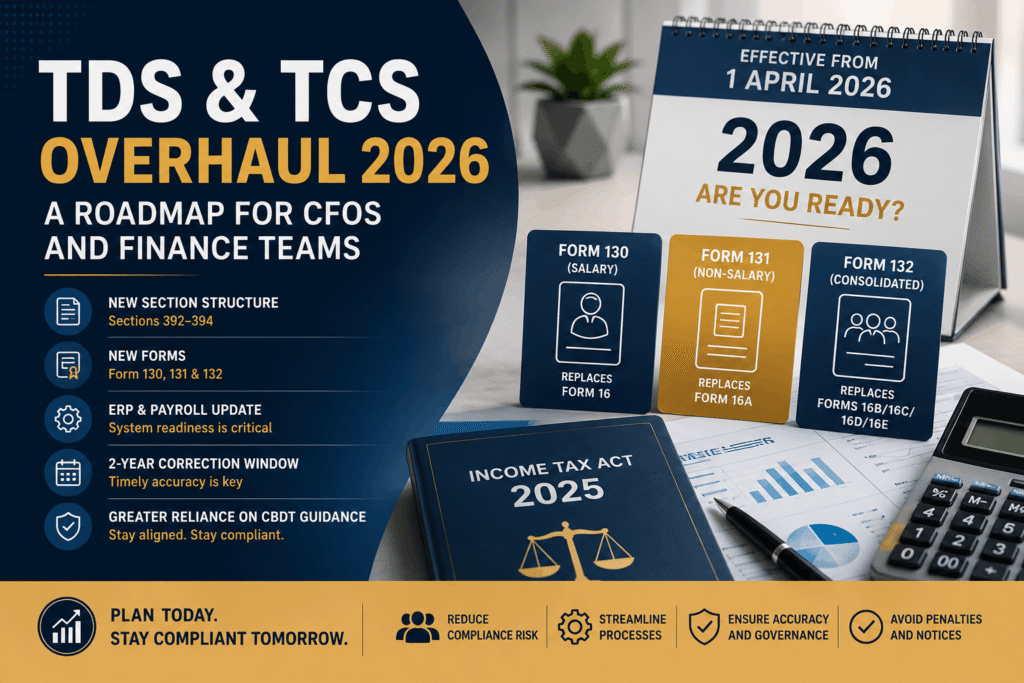

Several TDS and TCS provisions are expected to move under a reorganised chapter structure, including the proposed Section 392–394 framework for withholding taxes.

For businesses, this is not merely a drafting change.

Most accounting systems currently rely on existing section mapping such as:

- Section 192 – Salary

- Section 194C – Contractor Payments

- Section 194J – Professional Fees

- Section 206C – TCS provisions

Businesses using Tally, SAP, Oracle, Zoho, or customised ERP systems should evaluate whether their:

- deduction logic,

- challan mapping,

- vendor classification,

- and return preparation utilities

are aligned with the revised structure.

Why This Matters Operationally

If vendor masters or payroll configurations continue using outdated mapping logic, businesses may face:

- return validation issues,

- incorrect challan tagging,

- reconciliation mismatches,

- vendor disputes,

- or delays during quarterly TDS filings.

For larger organisations, even minor mapping errors may affect thousands of transactions in a single reporting cycle.

Form 16 Is Expected to Transition to Form 130

Another major operational change is the transition from existing TDS certificates to the revised form structure.

Under the proposed framework:

| Existing Form | Proposed New Form |

|---|---|

| Form 16 | Form 130 |

| Form 16A | Form 131 |

| Forms 16B/16C/16D/16E | Consolidated into Form 132 |

This means businesses may need to update:

- payroll software,

- employee tax documentation,

- vendor certificate generation,

- and compliance reporting templates.

Practical Example

Suppose an employee applies for a home loan in 2027 and submits salary tax documents to the bank.

Instead of the traditional Form 16, the employer may issue Form 130 under the revised framework. If payroll systems are not updated correctly, this may create confusion in documentation, reporting, or employee tax records.

Changes Finance Teams Should Monitor Closely

1. Manpower Supply Classification

Historically, businesses have faced recurring disputes regarding whether manpower-related payments should fall under:

- contractor provisions,

- professional services,

- or technical services.

The revised framework is expected to bring greater clarity in classification, particularly for manpower supply arrangements linked with Section 194C-type deductions.

This may affect:

- staffing companies,

- manpower contractors,

- security agencies,

- facility management businesses,

- and labour-intensive industries.

Businesses should review whether vendor categorisation in ERP systems remains aligned with revised compliance expectations.

2. Simplification in Certain TCS Categories

The revised structure also indicates movement toward simplified TCS rates in selected categories, including:

- overseas tour packages,

- Liberalised Remittance Scheme (LRS) transactions,

- and certain remittance-based collections.

Businesses dealing in travel, education remittances, overseas packages, or international transactions should monitor final notifications carefully before implementation.

3. Greater Reliance on CBDT Guidance

The revised framework is also expected to increase the practical importance of:

- CBDT circulars,

- departmental clarifications,

- and interpretational guidance

while evaluating withholding tax positions.

From a compliance perspective, businesses taking aggressive or unsupported tax positions may face higher scrutiny during assessments or departmental reviews.

For finance teams, documentation and internal justification may become more important than before.

The Two-Year Window for TDS/TCS Corrections

Another important procedural development is the proposed restriction on correction timelines for TDS/TCS statements.

The revised framework is expected to cap the correction window at two years from the end of the relevant financial year.

Why This Is Important

Many businesses currently:

- identify mismatches late,

- revise returns after audits,

- or correct vendor PAN/data issues much later.

A shorter correction window increases the importance of:

- accurate vendor onboarding,

- timely PAN validation,

- reconciliation reviews,

- and quarterly compliance monitoring.

For businesses handling high transaction volumes, delayed corrections may become significantly more difficult after the permitted period expires.

Areas Businesses Should Review Before April 2026

Rather than waiting for implementation deadlines, businesses may consider reviewing the following areas during FY 2025–26 itself:

Payroll & HR Systems

- TDS certificate generation

- employee declaration workflows

- salary deduction logic

- payroll utility updates

ERP & Accounting Software

- section code mapping

- challan configuration

- vendor deduction categories

- return filing compatibility

Vendor Master Review

- PAN validation

- deduction category accuracy

- contract classification

- historical mismatch review

Internal Compliance Processes

- maker-checker controls

- quarterly reconciliation

- correction tracking

- documentation standards

Who Should Take Professional Help?

Professional review may be advisable for:

- Companies with large vendor bases

- Businesses handling multiple TDS categories

- Organisations using customised ERP systems

- Startups with outsourced payroll functions

- Companies with prior TDS notices or mismatches

- Groups operating across multiple states/entities

- Businesses planning ERP migration or software upgrades

When Should Businesses Contact a CA or Compliance Advisor?

Businesses should ideally seek professional review if:

- payroll software has not yet been updated,

- vendor categorisation is inconsistent,

- TDS mismatches frequently arise,

- ERP systems rely heavily on old section mapping,

- or finance teams are uncertain about implementation impact.

Early review generally reduces the risk of last-minute reporting disruption.

Also Read

- New Income Tax Act, 2025

- Transfer Pricing Report

- LTCG on property Sale

- GST Registeration

- MSME Registeration

Frequently Asked Questions (FAQs)

What are the new TDS forms from April 2026?

Under the revised framework, Form 16 and Form 16A are expected to transition to Form 130 and Form 131 respectively.

Will existing TDS section codes change?

Yes, several withholding tax provisions are expected to be reorganised under a revised chapter structure in the new Income Tax framework.

Will businesses need ERP updates for the new TDS system?

Most likely yes. Businesses should review whether payroll systems, deduction logic, challan mapping, and reporting utilities remain compatible under the revised structure.

Does this affect small businesses using Tally or Zoho?

Yes. The impact is not limited to large SAP/Oracle users. Even businesses using Tally, Zoho, Marg, or customised accounting software may need compliance-related updates.

Can old TDS returns still be corrected later?

The revised framework is expected to impose a shorter correction timeline, increasing the importance of timely reconciliation and accurate filing.

Final Thought

The transition beginning from April 2026 is not only about new section numbers or renamed forms.

For many businesses, the real challenge will be ensuring that:

- payroll systems,

- vendor masters,

- deduction logic,

- and compliance workflows

continue functioning smoothly during the first reporting cycle under the revised framework.

Businesses that begin reviewing their systems early are likely to face fewer operational disruptions compared to those waiting for implementation deadlines.

Need Assistance Reviewing Your TDS & Payroll Readiness?

LUCKY GUPTA AND COMPANY – Chartered Accountant assists businesses with:

- TDS compliance review,

- payroll and ERP alignment,

- vendor reconciliation,

- compliance process evaluation,

- and transition support under the revised Income Tax framework.

Early system review can help businesses avoid reporting disruption during FY 2026–27 compliance cycles.