For ambitious businesses, global expansion is the ultimate milestone. Establishing holding companies in Europe, setting up manufacturing units across Southeast Asia, or operating dynamic subsidiaries in international hubs are standard paths to driving enterprise value.

However, recent landscape shifts across Indian regulatory bodies—including the Securities and Exchange Board of India (SEBI) and the Ministry of Corporate Affairs (MCA)—prove that cross-border corporate structures are receiving an unprecedented level of scrutiny.

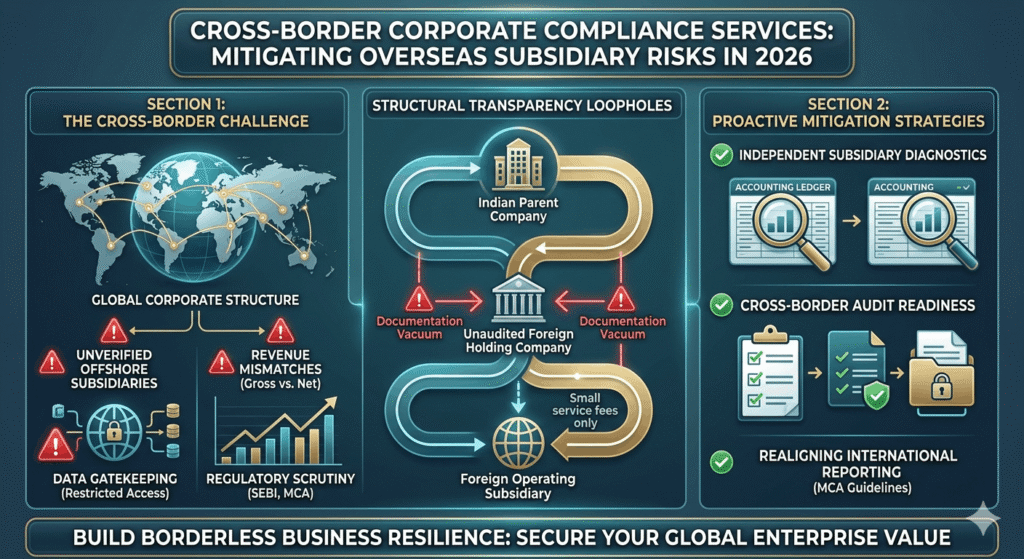

When an enterprise operates across borders, a standard consolidated financial report is no longer enough to satisfy stakeholders, lenders, or regulators. True business resilience requires deep, transaction-level visibility into every single foreign layer you build.

The Illusion of Consolidation: Why Surface-Level Accounting Fails

Many corporate leaders make a dangerous assumption: “If our global entities are integrated into our year-end consolidated financial statements, we are compliant.”

In modern corporate governance, this is a costly misconception. Regulators are increasingly looking straight through holding companies to verify the raw operations of the principal entities underneath.

Consider the dynamic between a holding company (an entity that exists primarily to own shares in other firms) and an operating company (the entity on the ground handling the actual physical manufacturing, refining, or logistics).

[Parent Entity in India]

│

[Unaudited Offshore Holding Layer] ──► Flags raised if gross revenues mismatch operational reality

│

[Foreign Operating Subsidiary] ──► Actual boots-on-the-ground service fees / revenue

If a foreign holding company recognizes the gross trading volume of physical goods on its balance sheet while the underlying operating refinery or factory only tracks a minor service processing fee, a massive structural mismatch is born. Without transaction-level records—like customs logs, local inventory risk profiles, and clear customer ownership documentation—this variance can be flagged as financial misrepresentation.

- The Compliance Impact: It is no longer acceptable to embed internally generated, unexamined financial records from unaudited offshore layers straight into a domestic listed framework. If a transaction cannot be independently verified by local forensic standards, your entire corporate group faces immediate reputational and valuation risk.

Need a structural review of your overseas entities? Relying on fragmented international advice can leave blind spots in your domestic reporting.Schedule a confidential evaluation with our senior cross-border advisory team today.

Structural Blind Spots: What Tripped Up Enterprises Historically

The stakes of cross-border compliance are higher than ever. Structural transparency issues that could historically be written off as minor international accounting disputes are now triggering significant corporate crises.

We see this risk landscape materialize across three distinct operational fronts:

1. The Data Gatekeeping Trap

When a domestic parent firm cannot—or does not—provide clear vendor lists, customer-wise sales data, or live accounting access for its overseas arms to local auditors, red flags go up instantly. Citing foreign data privacy laws or private client confidentiality agreements no longer shields an enterprise from local compliance mandates.

2. Inadequate Board Oversight across Jurisdictions

If public or institutional shareholders can see the final consolidated numbers but have zero line-of-sight into the financial statements of the individual sub-layers producing those numbers, investor confidence erodes.

3. Diverting Funds via Monitored Corridors

Parallel investigations regularly catch unapproved transactions where funds are shifted out of core corporate lines into promoter-controlled derivative trading accounts or unapproved investments.

The Broader Financial and Legal Impact

When a cross-border structural flaw is exposed by regulatory authorities, the downside is rarely confined to a simple fine. The knock-on effects can severely destabilize a healthy operating business.

┌─────────────────────────────┐

│ Regulatory Investigation │

└──────────────┬──────────────┘

▼

┌─────────────────────────────┐

│ Share Value Depreciation │ ──► Multiple consecutive lower circuits

└──────────────┬──────────────┘

▼

┌─────────────────────────────┐

│ Institutional Capital Flight│ ──► Major public funds force asset write-downs

└──────────────┬──────────────┘

▼

┌─────────────────────────────┐

│ Credit & Banking Strains │ ──► Commercial banks classify exposure as stressed assets

└─────────────────────────────┘

- Public Market Volatility: Regulatory interventions can cause immediate capital erosion, locking stock prices into consecutive daily lower circuits and wiping out retail and institutional wealth overnight.

- Institutional Asset Write-downs: Major domestic financial institutions holding significant equity stakes face heavy valuation adjustments, disrupting core investor relationships.

- Credit Crunch: Commercial banking partners do not wait for final court rulings. The moment an interim regulatory order highlights unverified revenues, banks aggressively classify corporate lines as stressed assets, freeze active working capital facilities, and initiate debt-recovery procedures.

How We Can Help: Protecting Your Global Enterprise Value

Expanding globally shouldn’t mean managing an opaque network of liabilities. Our comprehensive cross-border corporate compliance services bridge the gap between complex international operations and pristine domestic reporting.

We act as an integrated extension of your corporate governance framework by delivering:

- Independent Subsidiary Diagnostics: We trace your offshore financial flows, verifying that gross-to-net accounting transformations match the actual transfer of asset risks and rewards.

- Cross-Border Audit Readiness: We eliminate data gaps, ensuring that all foreign invoices, inventory trails, and client confirmations are structured to withstand rigorous domestic forensic audits.

- Regulatory Alignment: We realign your international entity reporting with current MCA guidelines, SEBI regulations, and relevant foreign reporting standards.

Secure your global architecture. Do not let unverified international layers threaten the enterprise you’ve built at home.Reach out to our specialists for an initial corporate health check.

Frequently Asked Questions

Can our company use international data privacy laws to withhold overseas transaction details from local authorities?

No. While foreign subsidiaries must respect local laws (such as Swiss banking secrets or GDPR in Europe), domestic regulators maintain that these agreements cannot dilute statutory transparency mandates for an Indian parent entity. If an overseas transaction directly impacts consolidated financial health, it must be accessible for independent regulatory verification.

What is the core difference between a trading holiday and a settlement holiday when executing cross-border capital transfers?

A trading holiday means market transactions are entirely suspended on the exchange. A settlement holiday means you can still actively buy or sell securities on the market, but the physical delivery of shares and transfer of cash are delayed because the commercial banks or clearing corporations are closed.

How does a gross vs. net revenue mismatch flag a corporate audit risk?

If a foreign operating unit reports modest standalone service revenues (net) while its holding entity claims massive transaction volumes (gross) without clear proof of asset ownership or inventory risk, auditors look at this as an optical revenue inflation risk. Every rupee of gross revenue must be backed by verifiable custody and risk documentation.

Also Read :

IFRS Consolidation Guide: Step-by-Step Process under IFRS 10 for Group Financial Statements

Received an Income Tax Notice Section 143(1)? Here is Your Practical Guide to Action

ROC Compliance Calendar FY 2026-27: The Corporate Governance Roadmap for Promoters